The jargon “backwardation” and “contango” purely exist in the futures market. A futures contract is technically a derivative agreement between the buyer and the seller. Here, the buyer agrees to buy the commodity from the seller sometime in the future at a predetermined price.

So, where do contango and backwardation fall into futures? And how can it help in understanding spot Gold price? Before we begin to understand the two terms, we need to have a basic idea of the market state.

Normal Market vs. Inverted Market

While in most cases, we get to see a normal or calm market, there are also instances of an "inverted" market that changes the trajectory of the futures contracts. A normal market is what you would imagine. The longer the contract between the buyer and seller goes on, the higher futures price.

On the other hand, an inverted market is the opposite of a normal market. The market experiences a situation where the underlying asset’s price is currently higher but will continue to decrease with a far-maturity or long-term contract. In both cases, the influence of the commodity's supply and demand sparks the beginning of either a normal or inverted market.

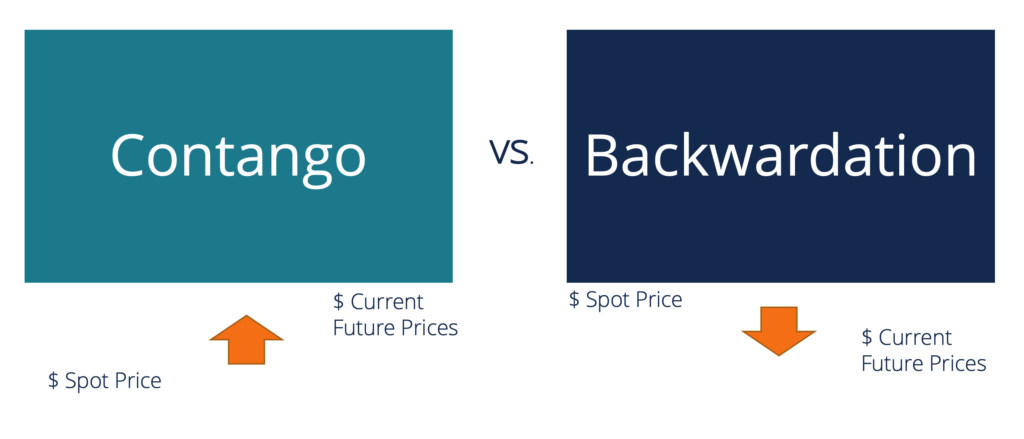

Contango Market

A contango market is essentially the same as the normal market, where the spot price is lower than the futures price. The futures price will continue to increase with time until the contract ends. The longer the contract, the higher the futures price will be. A one-year futures contract will have a higher futures price than a six-month-long contract.

With a gold futures contract in a contango market, it is more profitable to sell the commodity in a far-maturity contract or buy at a lower spot price to sell at a higher futures price. The contango market is a curve going upwards in a futures price graph.

Backwardation Market

A backwardation market is an inverted market where the spot price is higher than the futures price. It happens very rarely in the market and usually only lasts a short period of time. In a backwardation market, commodities like gold or silver are sold at a higher price during that short period of the inverted market.

After the period ends, the commodity price drops, resulting in a lower futures price. The backwardation market is a curve going downwards in a futures price graph. This market starts with higher demand for the commodity usually driven by scarcity or short term high demand. An economic or environmental crisis could cause such a situation. Periods of backwardation allow sellers, speculators, and short-term traders to sell the product at a much higher price.

How Does the Carrying Cost Affects the Price?

In a contango market, a long-term futures contract also means that the seller has to keep the underlying asset, which includes its cost of storage and security. When a contract is issued for a longer period, the seller can levy extra charges, leading to a higher futures price.

However, when a market is in a state of backwardation, the cost to carry is completely erased by the low-supply and high-value state of the market. The seller will benefit much more from selling the goods in the short term.

Conclusion

Understanding backwardation and contango and how it works can help determine the gold or silver price in the futures market. Looking for patterns of backwardation or contango can help an investor decide when to buy and when to sell their bullion.